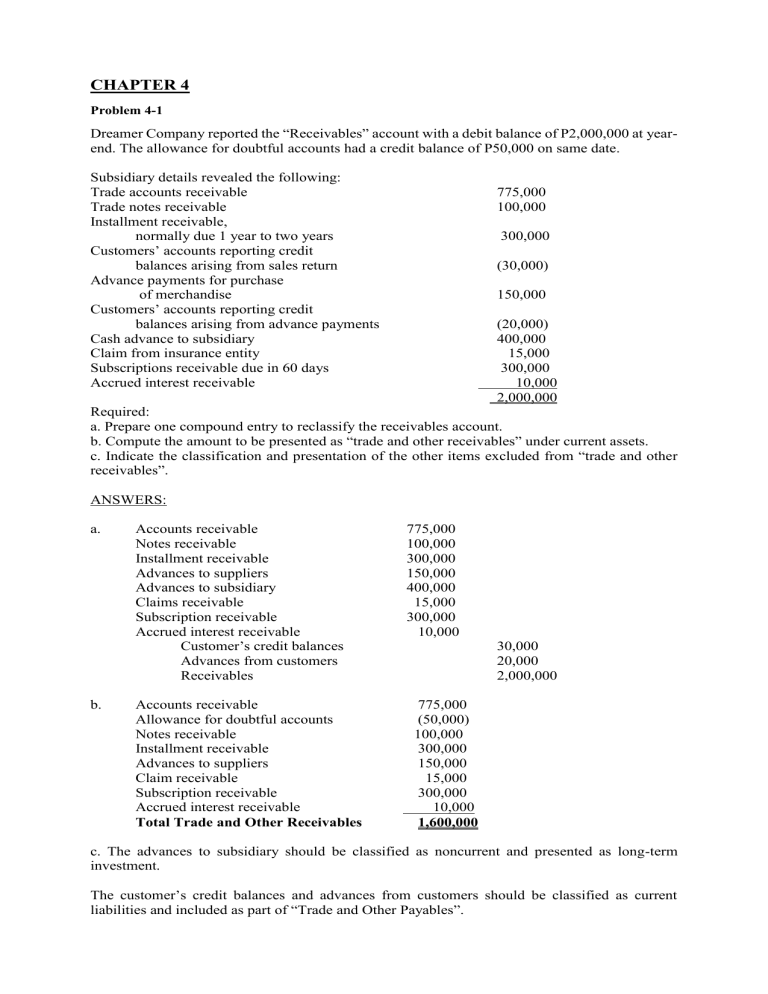

Once the identity suggests, jumbo finance is to own large mortgages to invest in a pricey home buy. In contrast to antique mortgage loans, jumbo fund try nonconforming because they exceed the most financing limits place by the Federal House Financing Agency (FHFA).

FHA Mortgage

FHA financing was mortgages supported by new Government Houses Administration. These are typically made to let first-time homeowners which will most likely not be eligible for a traditional financial get to the latest imagine homeownership. This type of home loans have more easy certification, such as minimal fico scores as little as five hundred and you will down payments as low as step three.5%. Regrettably, you can discovered a high interest than that have a conventional loan if the credit history otherwise down payment is lower.

Va Financing

The fresh new U.S. Agency from Seasoned Situations has the benefit of Va money in order to effective solution participants otherwise pros and you will eligible friends. These mortgage loans can be a reasonable choice when you have secure and you will predictable money and meet up with the qualification standards. Va financing don’t need a down-payment or personal financial insurance rates. Loan providers can get like a credit score out of 670 or more, though some accommodate reduced results.

USDA Colorado loan Sunshine CO Mortgage

USDA money can also be found and no money down. The fresh U.S. Department from Agriculture offers this type of financing to reduce-income borrowers in the being qualified outlying section.

Fixed-Rates vs. Adjustable-Price Mortgage loans (ARMs)

You will also have to consider if you need a predetermined-speed home loan or a varying-speed that and exactly how these could impression your own month-to-month funds. A fixed-rate of interest home loan is a good solution if you prefer an rate of interest and payment one to never change towards the lifetime of one’s financing.

In comparison, adjustable-price mortgage loans, or Arms, normally have a lowered initially interest with the first few many years, followed by an effective “floating” rates that goes up and you may drops that have sector criteria. If you’re a supply doesn’t give you the predictability of a fixed-price home loan, it could be of use if you are planning for the selling your residence till the initial rate of interest adjusts.

Financing Term

Ultimately, prefer that loan title one aligns together with your goals. Lenders usually cover anything from 10 so you can 3 decades, with extending for as long as forty years, however the most typical are a great fifteen- otherwise 29-season mortgage. You could potentially pick a shorter-term financial if you want to pay your house eventually and save well on focus will set you back throughout the years. Or, you may also prefer an extended-title home loan to lower your own monthly payments by distributed your mortgage harmony over a longer period.

5. Like a home loan company

Naturally, the majority of your notice might be into the finding loan providers providing the extremely advantageous rates and conditions, and also imagine additional factors, such as for instance charge and lender’s reputation.

- Apr (APR): The brand new apr ‘s the total price of credit, and additionally interest and you will fees. Looking around and you may evaluating ong several lenders makes it possible to get a hold of a knowledgeable harmony out-of Annual percentage rate, terminology and charge.

- Fees: Closing costs for funds are very different among lenders and you can generally range from 2% so you’re able to 5% of your amount borrowed, that total thousands of dollars. Which have good or expert borrowing, you’re able to discuss certain closing costs, like the origination commission.

- Reputation: View lender ratings, score web sites and you can friends’ suggestions to make sure the lender your like is actually credible. Think about, it is possible to rely on your own bank to grant direct preapproval info, while might work at all of them for a long time.

Issues to inquire about Mortgage lenders

Asking best concerns to mortgage lenders may help you influence a knowledgeable financial to invest in your property, like: